CA Vivek Agarwal

Financial reporting in India is passing through very remarkable moments owing to adoption of Indian accounting standards (Ind AS). Ind AS Implementation has very wide impact on the organization so companies should assess carefully impact on growth, strategies, joint ventures and tax planning. There are many challenges in implementation of Ind AS however this blog/ article focuses on 5 major challenges:

| Challenges Ahead Financial Instruments Deferred Taxation Revenue Recognition Control for Group Accounting Business Combination Financial instrument (Ind AS 32, 109):-There are no mandatory standards applicable under Ind GAAP, Ind AS provide the detailed guidance on accounting of classification, measurement, derecognition and impairment of financial assets and financial liabilities. The financial asset is classified based on entity’s business model for managing financial asset and contractual cash flow characteristics of the financial asset. Under an Indian GAAP, the classification of financial liability or equity is largely governed by legal form of the instrument and under Ind AS 32 the same is based on substance of the contractual agreement rather than its legal form. This may create the major changes in net worth as well as net income due to reclassification. |  |

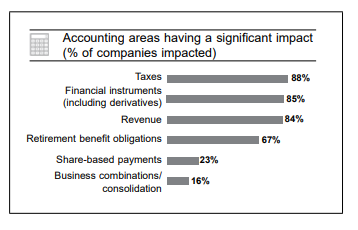

| Standard | Percentage of companies impacted |

| Financial Instruments | 83% |

| Income taxes | 87% |

| Property, Plant and equipment | 27% |

| Share-based payments | 22% |

| Business combination | 15% |

| Operating segments | 38% |

Source : Observation on Implementation of Ind-AS by EY

Key Differences

- Classification of liability and equity in case of compound financial instruments like convertible bonds, redeemable preference shares, compulsory convertible debentures etc.

- Re-classification of dividend and interest in profit & loss account due to reclassification of liability and equity.

- Expected loss model for Impairment of financial assets

- All derivative instrument to be carried at fair value, unless hedge accounting requirements met

- Investments to be categorized – Fair value through profit or loss, Fair value through other comprehensive income and amortized cost

Impact

Accounting Standards (AS) – 30, 31 and 32 were issued but not notified as there are constant changes in the accounting of financial instruments in International GAAP. ICAI had issued Guidance note on Accounting for derivatives applicable for accounting period commencing after 1st April 2016 for Non-Ind AS entities. However, there is a significant diversity in the practice. The implementation of Ind AS 32, 109, disclosure requirements of Ind AS 107 and applying fair value measurement of Ind AS 113 would be the most challenging during Ind AS Implementation. As per various reports, it is observed that Standards relating to Financial Instruments are the most challenging standards.

Control /Consolidation (Ind AS 110) Under prevailing accounting standard control is assessed on the basis of more than one-half of the voting power or control on the composition of board however as Ind AS is principle based standard, it explains the control in detail and Ind AS 110 provides a single control model.

As per Ind AS 110, “An investor controls an investee if and only if the investor has all the following:

- power over the investee ;

- exposure, or rights, to variable returns from its involvement with the investee; and

- the ability to use its power over the investee to affect the amount of the investor’s returns”

The determination of who controls whom is the critical when we move from existing Indian GAAP to Ind AS. The universe of entities that get consolidated could potentially different under both the frame works. The application of control definition would change the line items of Consolidated financials in Ind AS.

Key Differences

- Consolidation based on new definition of control

- Veto right with minority share holders

- Potential voting rights

- Structured entities

- De facto control

- Deferred tax on undistributed reserve

- Deferred tax on intercompany elimations

- Mandatory use of uniform accounting policy

Impact

With the introduction of new definition several entities that are not currently consolidated may get included and vice-versa and it will be a challenge for Corporate India and professionals.

Revenue recognition (Ind AS 115)

Ind AS 115, Revenue recognition from contract with customers, introduce a single revenue recognition model, which applied to all type of contracts with customers, including sale of goods, sale of services, construction arrangements, royalty agreements, licensing agreements etc. In contrast under existing Indian GAAP, there is separate guidance that applies to each of these type of contracts. Ind AS brings five-step model which determines when and how much revenue is to be recognized.

Key Differences

- 5 step revenue recognition model

- Timing of recognition of revenue (Right of return, dispatch Vs. delivery) based on satisfaction of performance obligation

- Detailed Guidance on

- Incentive schemes

- Service concession arrangements

- Customer loyalty programs

- Time value of money to be considered

- Separation of contracts in case of linked transactions

Impact

India has adapted Ind AS 115 and it has impacted the Real estate industries with partial completion vs completion method very highly.

Business combinations (Ind AS 103)

Currently there are no comprehensive standard which wholly addressing accounting for business combination, currently it is done by form of transaction like Merger, Acquisition etc. Under Ind AS 103, all business combinations are accounted for using the purchase method that considers the acquisition date fair values of all assets, liabilities and contingent liabilities.

Key Differences

- Acquisition date is the date when control is transferred – not just a date mandated by court or agreement

- Mandatory use of purchase method of accounting and fair value

- Post-acquisition amortization of asset based on the acquisition date fair values

- Transaction cost charged to the profit and loss account

- Goodwill to be tested at least annually for impairment

- Common control transactions are accounted using pooling of interest method

Impact

With the adoption of new requirements on business combinations, it will result into consistency over the period. Companies which are in progress of negotiation regarding acquisition, need to pay kind attention to the requirement of the standard. Fair valuation of asset on the date of acquisition and resultant goodwill are major areas to look after under new Ind AS.

Deferred taxes (Ind AS 12)

As per Indian GAAP deferred taxes are recognized on timing difference between accounting income and taxable income for the year and it is known as income statement approach whereas under Ind AS, deferred taxes are recognized for future tax consequences of temporary differences between carrying value of assets and liabilities in their books and their respective tax base and known as balance sheet approach.

Key Differences

- Ind AS is based on balance sheet approach whereas AS 22 is based on income statement approach

- Disclosure requirements are more detailed in Ind AS compare to AS

- Deferred tax on revaluation, undistributed profit by subsidiaries/associates, inter company elimination

- The concept of virtual certainty does not exist in Ind AS 12

Impact

Whole method of calculation of deferred tax provision has changed so we have to carefully assess the impact on the financial statement. On transition to Ind AS, the deferred tax on reconciliation with Ind AS, deferred tax on components of Other Comprehensive Income (OCI) and during consolidation will be challenging during implementation.

The above mentioned are some of the major challenges in implementation of Ind AS. The other areas of challenges are application of Ind AS 101 First time adoption, determination of functional currency under Ind AS 21, preparation of Statement of Changes in Equity and accounting of components of Other Comprehensive Income. Corporate India and professionals have to be cautious while dealing with transformation process to ensure smooth and effective convergence.

(Source: This article is published in souvenir of National Convention 2023 which was held on 23rd & 24th December 2023 at Kolkata)